The Home Loan Process

Financing Your Home Purchase

Navigating the financial landscape of buying a home can be overwhelming, but at Vis Realty Group, we’re here to help simplify the process. Understanding your financing options is crucial to making informed decisions that align with your budget and goals.

Explore Your Options

When it comes to financing your home, there are several avenues to consider:

1. Conventional Mortgages:

These are traditional loans not insured by the federal government. They typically require a higher credit score and a down payment, but they often have competitive interest rates.

2. FHA Loans:

Backed by the Federal Housing Administration, these loans are designed for low to moderate-income buyers. They feature lower credit score requirements and down payments as low as 3.5%.

3. VA Loans:

If you’re a veteran or active-duty service member, you may qualify for a VA loan. These loans require no down payment and offer favorable terms, making homeownership more accessible for those who have served our country.

4. USDA Loans:

If you’re looking to buy in a rural area, a USDA loan might be right for you. These loans require no down payment and are focused on helping low to moderate-income buyers.

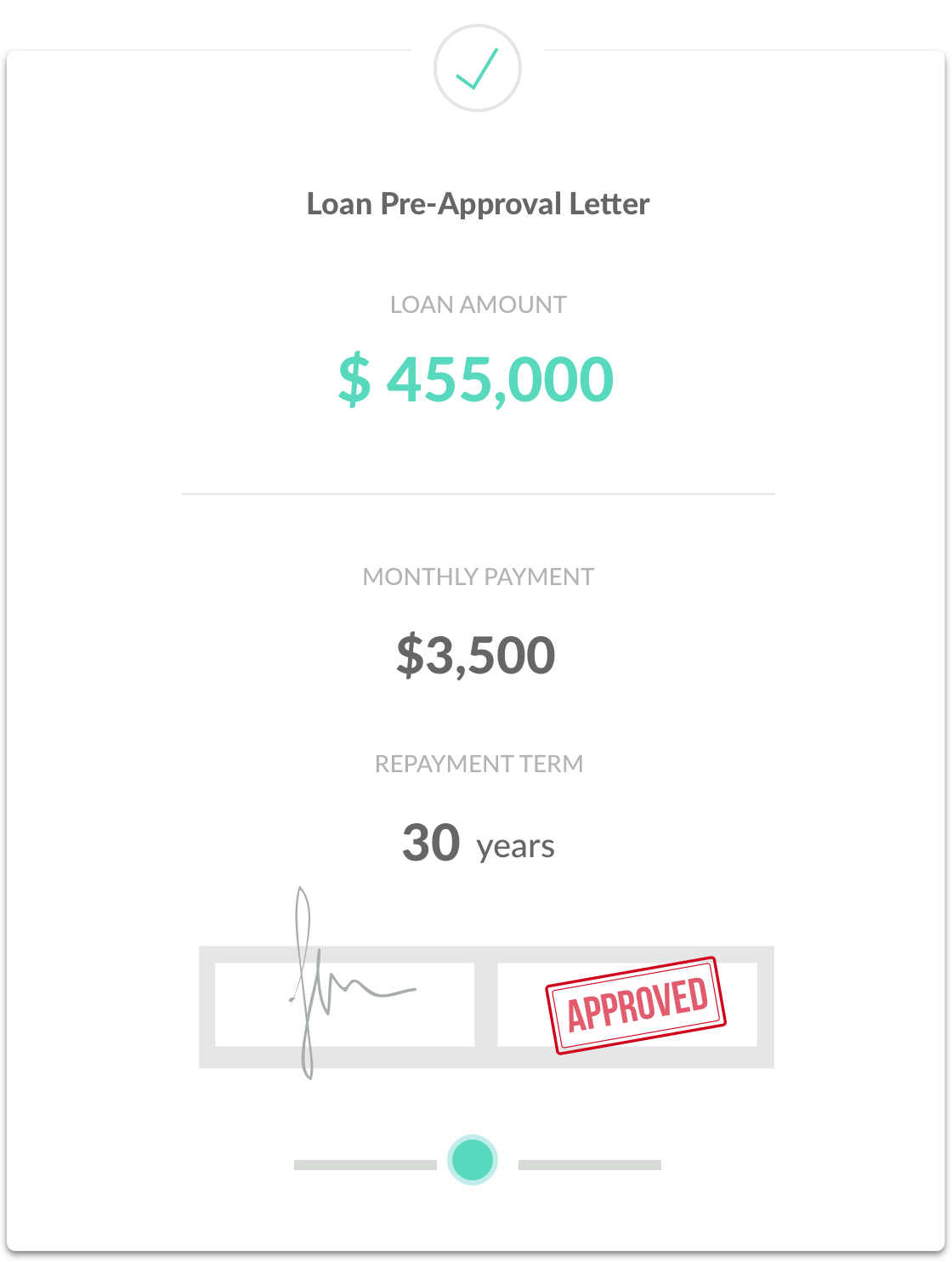

Getting Pre-Approved

Before you start your home search, obtaining pre-approval from a lender is essential. This process not only helps you understand how much you can afford but also strengthens your position when making an offer. Our network of trusted lenders can guide you through pre-approval, ensuring a smooth start to your home buying journey.

The Importance of Budgeting

Create a budget that includes not just your mortgage payment, but also property taxes, insurance, maintenance, and utilities. Understanding all potential costs will help you manage your finances effectively and avoid surprises in the future.

We’re Here to Help

At Vis Realty Group, our experienced agents are dedicated to helping you navigate your financing options. We’ll provide you with the resources and guidance needed to make informed decisions.

Ready to take the first step toward financing your new home? Contact us today to learn more about your options and how we can support you throughout the buying process. Your dream home awaits!

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

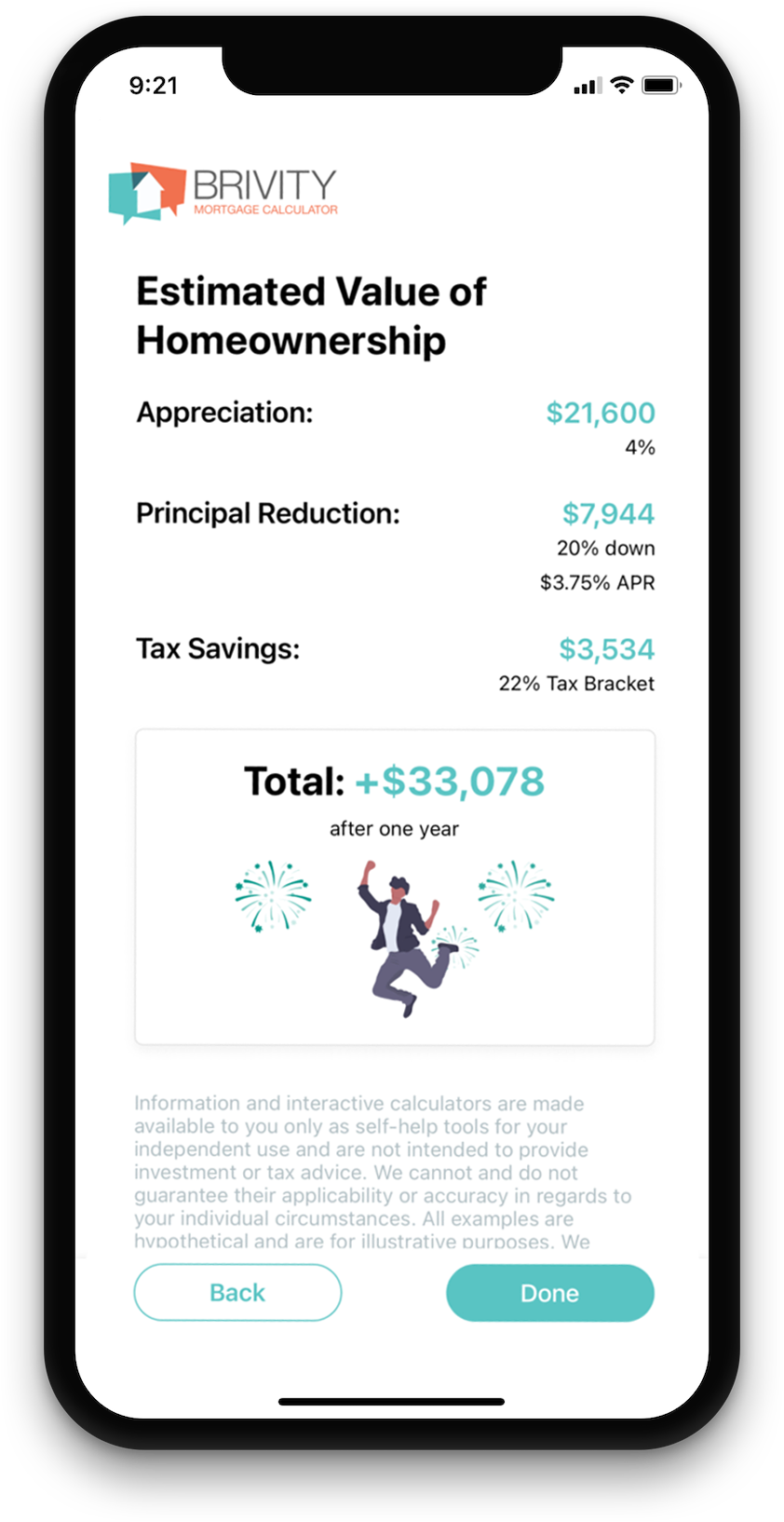

ESTIMATE YOUR MONTHLY PAYMENT

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)We Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!